Edition 6

Oct 30, 2025

Your Business Snapshot:

India’s microfinance engine is stuttering: delinquencies near 6 per cent, tougher competition from small finance banks and NBFCs, regulatory shifts and weaker rural incomes are squeezing margins

With the US shutdown dragging into late October, contractors go unpaid, FDA and SEC bottlenecks stall drug approvals and IPOs, small suppliers face cash crunches amid a data fog, and only pockets of airline resilience offset rising uncertainty.

Beijing is accelerating renminbi internationalisation by widening foreign access to onshore markets and using Hong Kong as a funding hub, lifting the RMB share of global trade finance to about 7.6 percent while the dollar remains dominant.

AI’s biggest players are recycling the same capital through overlapping chip, cloud and compute deals, creating a self reinforcing revenue loop that drives eye watering valuations while concentrating risk in a handful of firms.

Economics

What higher delinquency rates mean to the Indian micro-finance industry and its economy?

Microfinance, namely popularised by Grameen Bank in Bangladesh is the provision of financial services such as small loans or saving accounts to low-income families often found in LIC’s who are unable to access formal banking. This model of financial banking is aimed to help small businesses and people to become more self-sufficient, giving them an opportunity to build enterprises and access crucial credit. By promoting financial inclusion, this could help reduce the wealth gap and absolute poverty within the Indian economy, further raising the standard of living for the Indian population.

Delinquencies across India’s microfinance borrowers have since doubled to 6%[1], while the loan book has been shrinking, pointing to greater concerns over default risks. Other socio-political and geographical factors have also contributed to this. In 2018, India’s Supreme Court banned the use of Aadhaar, the national ID system which is used for loan verification. This increased the hurdles for many Indians borrowers who no longer have a centralised system to gain credit and trustworthy financial loans. In 2022, the Reserve Bank of India passed the Regulatory Framework for Microfinance Loans which created a single rule-set for all regulated lenders, allowing households to take up to 50%[2] of household income and also take loans from multiple providers. SFB’s (Small Finance Banks) and NBFCs (Non-Banking Financial Companies) entering the market reduces profit margins and pricing power. Coupled alongside the reduction of real rural wages from 2019 to 2024 by 0.4%, income stagnating and food prices rising.

How has the arrival of new competitors (SFB’s and NBFC’s) into the microcredit industry impacted India’s economy? India’s market prior to the introduction of RBI regulation, was predominantly dominated by MFIs (non-bank lenders focused on small and unsecured loans). MFIs have since been pressured by the higher competition and higher credit costs as delinquency rates have risen by 6%, further reducing profit margins. This is reflected through a 75%[1] year on year drop in quarterly profits as more and more loans have defaulted or soured. As a result, it creates knock-on effects as lenders' cost of money increases, passing on these extra costs to consumers through higher rates. Rising delinquencies takes away provisions and funding costs for micro-lenders, forcing less money to be loaned out to households and small businesses. Therefore, lower spending within the Indian communities and households could reduce consumption for local goods, potentially having drawbacks on the economic growth of India.

Business

The US government shutdown takes it toll on businesses

The U.S. federal government shutdown, now stretching into late October, is hitting companies squarely, especially those tied to federal funding or regulatory oversight. Financial Times reports show that federal contractors are among the hardest hit. Payments for ongoing work are delayed, and new contracts are put on hold. Companies like Lockheed Martin, Boeing, Oracle and SAIC face serious cash‑flow pressures, project delays and even potential layoffs for their employees, some of whom aren’t guaranteed back pay[3].

Pharmaceutical and biotech firms are also struggling as the Food and Drug Administration operates with limited staff. This means that new drug approvals, clinical trials, and medical device reviews are taking much longer than usual. Smaller firms, often relying on quick decisions to launch or keep going, are left in limbo, uncertain when or if they’ll see any progress on their applications. These bottle-necks aren’t just shuffling papers; they’re leaving new lifesaving products and company revenues on hold[5]. The shutdown’s impact reaches Wall Street as well. The Securities and Exchange Commission is working with a reduced team. As a result, companies hoping to launch an IPO or raise capital are facing backlogs. Financial industry leaders have warned this creates major uncertainty for business planning and could slow investments across a wide range of sectors. Deals are being put off, and companies are struggling to make future plans with so much unpredictability[4].

Some sectors have shown resilience. For example, despite worries about air traffic control staffing, Delta Air Lines reported strong quarterly results and stated that they’ve managed to avoid significant disruptions so far. Other airlines like Boeing, however, could face increased risks if the shutdown drags on and safety inspections or regulatory approvals get delayed[4].

Smaller businesses, many of which depend on steady federal contracts, are in a much more precarious position. The government normally pays out hundreds of millions for contracted services every day. With those payments frozen, small business owners are under real financial pressure to pay their staff and cover expenses out of pocket, with no clear end in sight[3]. Another problem is the lack of government data. Important reports about employment, inflation, or consumer spending are delayed, so business leaders don’t have the numbers they need to plan ahead. This “data fog” adds even more uncertainty, making it harder for management teams to forecast demand, set budgets, or make decisions on hiring and investment[6].

The government shutdown isn’t just a headline—it’s a day-to-day challenge for contractors, pharma companies, financial firms, airlines, and small businesses alike. What started as a political deadlock has now become a real business struggle, creating delays, cash flow issues, and new risks for companies across the board.

Markets

China’s renminbi push moves from ambition to traction

China’s central planners have made it clear: they want the renminbi (RMB) to matter on the world stage, especially in trade and sovereign credit, because growing currency usage strengthens China’s economic position.

China wants to de-dollarize; “a dollar-based system is inherently unstable and has disadvantages that a multicurrency system would not have” furthering Beijing’s desire to move away from a dollar-based global monetary system to a multi-polar one. As part of this campaign, China is opening more channels for foreign investors to buy renminbi-denominated bonds as well as expanding the use of the renminbi overseas through a network of offshore clearing banks[1]. External renminbi loans, deposits and bond investments by Chinese banks quadrupled to more than Rmb3.4tn ($480bn) over the past five years. Recent data from China’s State Administration of Foreign Exchange shows the external fixed-income assets of Chinese banks more than doubling over the past decade to more than $1.5tn, with the share denominated in renminbi expanding rapidly to almost $484bn at the end of June. This includes $360bn of renminbi loans and deposits, up from $110bn in 2020[7].

Policymakers are moving to address this. Hong Kong authorities have embarked on a plan to make the city a hub for fixed income and currency trading. Simultaneously, Beijing has opened its domestic interbank repo market to foreign investors, allowing them to use renminbi fixed-income assets as collateral for renminbi loans, “It only makes sense for investors to allocate more into these assets if they are able to use them for more than just holding and generating an income”. A big part of the expansion in RMB lending has been in trade finance. For instance, the renminbi’s share of global trade finance quadrupled over the past three years to 7.6% in September, making it the second most-used currency in trade finance after the US dollar[7].

For trading partners, exchanging with China means lower cost, fewer currency conversions, and potentially different financial risks. Furthermore, this could create a shift from the current dependency on the US as economies become financially tied to China giving it more influence and soft power. Some countries already adopted trading in RMB, for instance sovereign borrowers including Kenya, Angola and Ethiopia have converted old dollar debts into renminbi this year.

However, the dollar is still dominant. More than 90% of global foreign exchange transactions are in dollar while The RMB’s share in global trade finance is still small around 8%[8].

Tech

Circular AI Deals: A Symbiotic Strategy or Signs of a Bubble?

Money is echoing through Silicon Valley. Each dollar spent on chips, cloud storage, or compute power seems to bounce back through the same handful of firms. This loop of investment and revenue has supercharged growth, but some investors worry it’s beginning to sound like a bubble.

According to The Wall Street Journal, AI leaders such as Nvidia, Microsoft, OpenAI, Oracle, and CoreWeave are tied together through billions in overlapping contracts and investments[9]. Nvidia supplies chips to Microsoft and CoreWeave; Microsoft powers OpenAI through Azure; and OpenAI, in turn, has agreed to purchase $300 billion worth of computing power from Oracle over five years. These connections, visualised in recent data from The Wall Street Journal, illustrate just how tightly the AI ecosystem has become intertwined.

Supporters argue that these arrangements are a natural response to AI’s enormous infrastructure demands. Data centres cost billions to build, energy requirements are soaring, and the speed of model development requires long-term partnerships to ensure stability.

Analysts at J.P. Morgan described these deals as capital-efficient risk management; a way to secure compute power and liquidity without relying solely on external investors[10].

But there is growing concern that this circularity could be masking vulnerabilities. When the same handful of companies drive both demand and supply, valuations can become self-reinforcing. Nvidia, for example, briefly reached a market cap of $4 trillion this summer, fuelled in part by orders from firms whose operations depend directly on its hardware and, indirectly, on its share price. The BBC recently noted that investor optimism toward AI has lifted valuations to levels not seen since the late 1990s tech bubble[11].

The numbers themselves are impressive, but the concentration of risk is equally striking. Most AI profits are being captured by a few dominant firms, and if the economics of AI training or energy usage shift, these relationships could unravel quickly. Yet, unlike previous bubbles, today’s AI demand is grounded in real infrastructure including data centres, chips, and enterprise software.

Still, the question remains: when the same dollars circulate between the same players, how sustainable is the growth? Whether this represents a new model of industrial coordination or an early warning of market excess will define the next chapter of the AI story.

Bonus Section

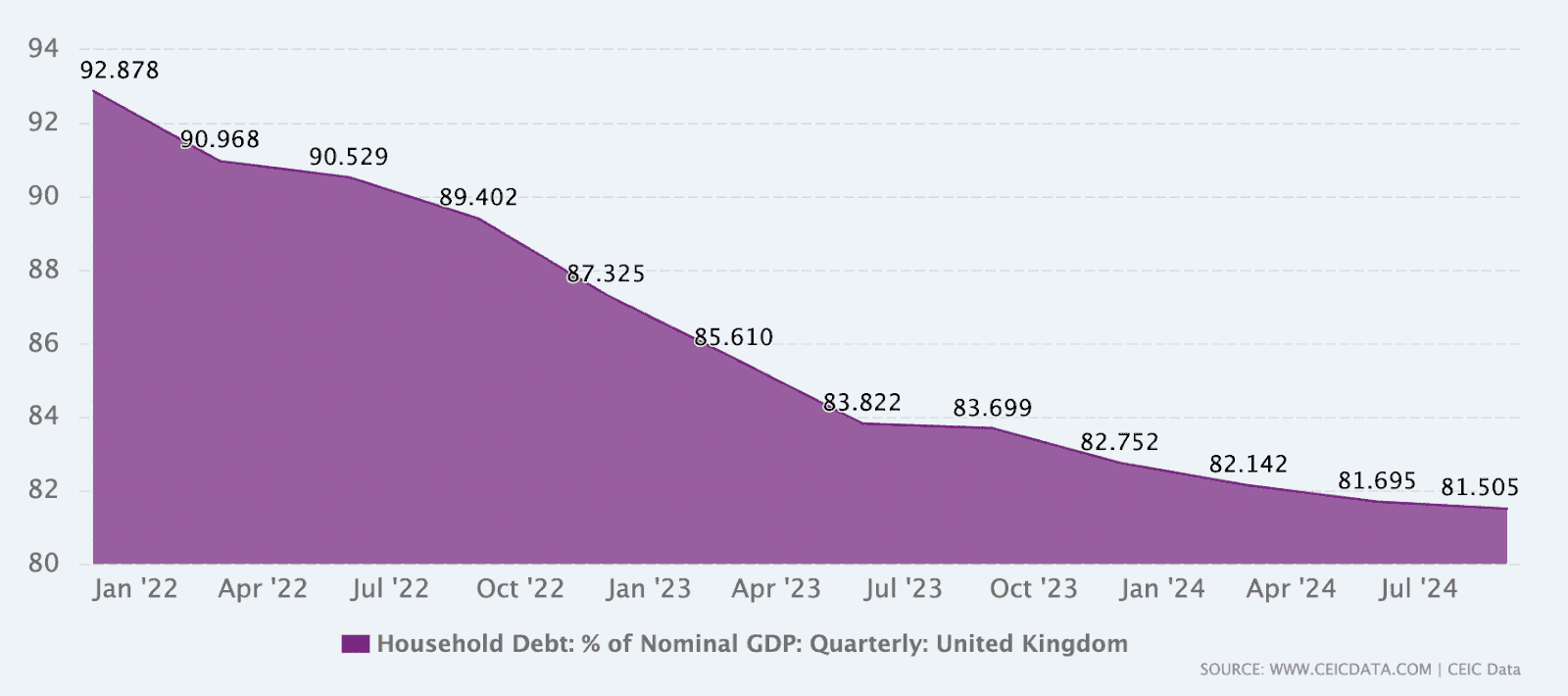

Chart of the Week: Household Debt, Productivity & Credit

[13]CEICdata.com, 2025

Recent data puts the spotlight squarely on three structural challenges in the UK economy.

Household debt remains elevated at ~81.6 % of GDP, down from the 2010 peak but still historically high[13].

Labour productivity growth has stalled, output per hour increased just 0.2 % in Q1 2025, weakening from 0.7 % in Q4 2024[14].

Consumer credit is rising again: unsecured borrowing is climbing, adding pressure on household finances[15].

Why this matters:

High household debt reduces consumer resilience in the face of inflation or rate rises, meaning weaker spending when it matters.

Slow productivity translates into slower wage growth, less corporate investment and muted economic growth, especially relevant for students entering the job market.

Elevated consumer credit signals that many households may be substituting debt for income growth, which isn’t sustainable in an economy with weak productivity.

Editors: Liam Sanderson, Dinel Gamage

Writers: Saaina Bajaj, Filip Wang, Cleo Vuillot, Harshil Nichani

References:

[3] FInancial Times - https://www.ft.com/content/bea47bf7-b54a-4d46-a7f7-3a6ce531329a

[4] Financial Times - https://markets.financialcontent.com/ibtimes/article/marketminute-2025-10-14-government-shutdown-casts-long-shadow-over-economy-and-interest-rate-outlook-ahead-of-powells-pivotal-speech

[5] Investopedia - https://www.investopedia.com/shutdown-s-economic-risks-grow-as-it-drags-on-11833907

[6] Financial Times - https://markets.financialcontent.com/ibtimes/article/marketminute-2025-10-2-federal-shutdown-stalls-inflation-data-blurring-feds-path-and-rattling-markets

[7] Financial Times - https://www.ft.com/content/4577100f-8b71-4647-8e7e-fead115d9552?utm_source=chatgpt.com

[8] Bank for International Settlements - https://www.bis.org/publ/qtrpdf/r_qt2212x.htm

[9] WSJ – https://www.wsj.com/tech/ai/is-the-flurry-of-circular-ai-deals-a-win-winor-sign-of-a-bubble-8a2d70c5

[10] J.P. Morgan (2025) – https://am.jpmorgan.com/us/en/asset-management/adv/insights/market-insights/market-updates/on-the-minds-of-investors/does-circularity-in-ai-deals-warn-of-a-bubble/

[11] BBC (2025) – https://www.bbc.co.uk/news/articles/cz69qy760weo

[12] Chart Source: Wall Street Journal – “Is the Flurry of Circular AI Deals a Win-Win—or Sign of a Bubble?”, 2025.

[13]Ceic Data - https://www.ceicdata.com/en/indicator/united-kingdom/household-debt--of-nominal-gdp?utm_source=chatgpt.com

[15]Trading Economics - https://tradingeconomics.com/united-kingdom/consumer-credit