Edition 5

Oct 23, 2025

Your Business Snapshot:

The Fed is preparing to end quantitative tightening to stabilise bank reserves and money markets, aiming to keep overnight rates anchored and make the pass through to mortgages and small business credit more predictable.

S&P is buying With Intelligence for about $1.8 billion to secure private markets data, unlock new indices and analytics, and strengthen its competitive position, with earnings uplift targeted by 2027.

Global equities advanced as Japanese political stability, firmer Chinese growth, solid US earnings and resilient emerging markets combined to lift risk appetite across regions.

Netflix will host select Spotify video podcasts from early 2026, while Spotify outlines a label backed plan for responsible AI tools in music.

Economics

Fed seen nearing a halt to balance-sheet drawdown as market plumbing strains.

The Federal Reserve is set to end quantitative tightening (QT) as short-term funding markets show signs of stress and policymakers seek to preserve a smoother rate control. QT has reduced the Fed’s assets from a pandemic peak of near $9 trillion to roughly the mid-$6 trillion mark, reducing bank reserves and tightening liquidity conditions[1]. Recent jumps in repo benchmarks indicate that reserves may be approaching the ample threshold below the rate volatility tends to rise. This could have knock-on effects on everyday borrowing for households and consumers. Mortgage quotes can become even more volatile with some adjustable loans resetting higher, while smaller businesses may face tighter bank lending and wider spreads on working-capital or equipment loans.

Fed Chair Jerome Powell said on Oct 14 that the end of balance-sheet runoff ‘may be nearing,’[2] noting firmer repo rates and occasional money-market pressures. This further reaffirms the Fed plans to stop QT. The main concern is if reserves become too scarce, overnight rates can move away from the policy target. This may lead to banks storing up liquidity, and credit conditions can tighten even without a change in the policy rate. Halting QT would aim to stabilise reserves so that the transitions from policy decisions to household and business borrowing remains relatively predictable.

The Fed aims to avoid an unintended additional tightening from market plumbing on top of its policy stance. The balance sheets have fallen substantially during the pandemic peak and therefore the Fed wants to stop before reserves run low. A halt in quantitative tightening is not designed primarily to stimulate demand, it is more intended to preserve smooth policy transmission by preventing reserve scarcity and volatility in overnight rates. Therefore, changes in policy flows predictably to mortgages and business credit[2].

Business

S&P to acquire With Intelligence

Last Wednesday, S&P Global, the U.S. financial-data giant best known for the S&P 500 index and credit ratings, announced the acquisition of the London-based data and research company With Intelligence for $1.8 billion. Even though S&P did not disclose financial terms of the transaction, the deal is expected to close in late 2025 or 2026 due to regulatory approvals[3].

Firstly, the deal is likely to facilitate access to the fast-growing private market segment and therefore exposure to a vast amount of proprietary data from private capital groups. Its goal is to “deliver deeper insights, stronger connectivity and greater transparency across the private markets ecosystem”. With Intelligence was founded in 1998 and serves more than 3000 clients. Moreover, the company has large datasets about private equity, real-estate funds, hedge funds and the relationships between investors such as LPs and fund managers like GPs[4]. That data isn’t easy to get because private markets are often more opaque. Buying them instantly gives S&P access to proprietary data from 34,000 private equity groups, 19,000 real estate investors and 17,000 hedge funds, along with thousands of other private capital groups. For instance, the company recently announced plans to launch an index tracking the top 50 private equity funds, in collaboration with fintech group NewVest.

Secondly, this deal empowers S&P to improve products and margins. While With Intelligence brings benchmarks, workflow tools and relationship data, S&P brings scale, distribution, analytics, and brand trust. Together they can build new products such as private-markets indices, performance analytics, unified platforms and sell them to banks, pension funds, GPs and LPs. The combination aims to improve cross-selling opportunities and should generate cost and revenue synergies over time. The company is expected to increase its profit per share by around 2027[5].

Finally, the sale also marks a profitable exit for With Intelligence’s majority owner Motive Partners, a financial technology-focused private equity group, as well as the minority investor ICG and the company’s management[6].

Overall, S&P’s acquisition of With Intelligence strengthens its competitiveness against its main rivals such as Moody’s, MSCI, and Morningstar by protecting its leadership in financial information.

Markets

Global markets rally on policy optimism

The recent Global financial markets have seen a strong, optimistic start to the week, as a series of positive signals from leading economies and policy developments have driven gains across major stock exchanges. In Japan, the Nikkei 225 surged to a new record, closing up nearly 3% at 48,970.40. This rally was set in motion by the news that the Liberal Democratic Party was able to form a coalition with the Innovation Party, ensuring broad political stability and clearing the way for Sanae Takaichi to become Japan’s first female prime minister. Investors in Tokyo and abroad embraced the expectation of continued government stimulus and its monetary policy, especially as the new administration is seen as likely to support pro-business reforms aimed at sustaining growth after years of sluggish inflation and pandemic disruption. The surge in Japanese equities had ripple effects worldwide[7][8].

European stocks tracked the upward momentum, with the FTSE 100 and other major indices in London mirroring the bullish sentiment seen in Asia. The optimism was further fuelled by strong economic data from China, where their third-quarter GDP growth of 4.8% year-on-year beat market expectations and industrial production jumped 6.5%. These figures helped reassure global investors that China’s demand for exports, commodities, and technology remains solid, even as the country’s property sector continues to lag. This improved outlook from China, the world’s manufacturing hub, also gave a boost to commodity-linked stocks and helped lift European and American multinationals that depend on Chinese end-markets[9][10].

Turning to the United States, the S&P 500 enjoyed its strongest week since early August as robust earnings from major banks and tech sector leaders revived investor risk appetite. The rally in the US was further supported by waning concerns around the US–China tariff standoff and hopes that the Federal Reserve may be nearing a peak in its interest rate tightening cycle[9][10]. Meanwhile, in India, markets hit new highs with the Nifty50 breaking through the 25,900 mark and the Sensex up over 650 points, thanks to festive trading and strong bank and consumer sector results. Throughout emerging markets, performance has been robust, with the MSCI Emerging Markets Index posting its best year-to-date run in more than a decade as demand for higher yields and better local currency performance continues[11][12].

Momentum broadened from Tokyo to London and New York, underpinned by Japanese political clarity, stronger Chinese data and upbeat US earnings alongside hopes the Federal Reserve is near its peak rate. The rally now turns on whether incoming inflation and growth readings can validate this renewed risk appetite.

Tech

Spotify and Apple announce major shifts in the entertainment space

Large firms have continued to expand into live entertainment, with Apple announcing a deal for the US Formula 1 rights. This has come with a flurry of tech announcements and partnerships that aim to ignite the media sector. Netflix and Spotify have announced collaboration on podcast streaming, Netflix have also secured a deal with WWE, Spotify have started developing a platform for AI music generation and Meta have announced an expansion of Threads boosting their portfolio of services.

Apple’s announcement includes a $700mn deal for the US Formula 1 streaming rights, previously held by ESPN, which marks another development in the region with its growing F1 fan base[13]. Apple has already witnessed the appeal of F1 following the success of its production of ‘The F1 Movie’, with the hopes that this new deal will bring 1.4 million existing US customers to the Apple TV platform. This increases the offering of Apple TV who have also seen wild success with the TV show Severance this year in a challenge against some of the much larger streaming services. Separate from its role in the entertainment industry, Trump's recent tariff announcement threatened their capacity to produce in China, however news last week has brightened the dampened investor outlook. The Financial Times revealed that the new Iphone 17 has kickstarted the strongest growth in Iphone sales since Covid-19, which in combination with its F1 deal helped the firm’s stock price rise 1.2% on Friday[1].

Spotify has also made major announcements in the tech space. They have detailed a partnership with Sony, Universal and Warner, which brings it further into the AI music space, along with an announcement with Netflix to stream podcasts. The former outlines a scheme to produce AI products, with the construction of a new AI lab and research team. Spotify has already introduced an AI DJ and AI Playlist features, however this only affects how listeners receive music, not how the music is actually created[14]. This could spark many controversies in the industry, with the role of AI generated music being a hotly contested topic and seen as a threat to many big name artists[14]. The latter announcement aims to expand Netflix's product choice and unlocks a new distribution opportunity[15].

Overall, the tech developments of both Apple and Spotify are just two of the many drastic moves in the entertainment space that increase product portfolios, expand on AI use and give tech firms a new revenue stream.

Bonus Section

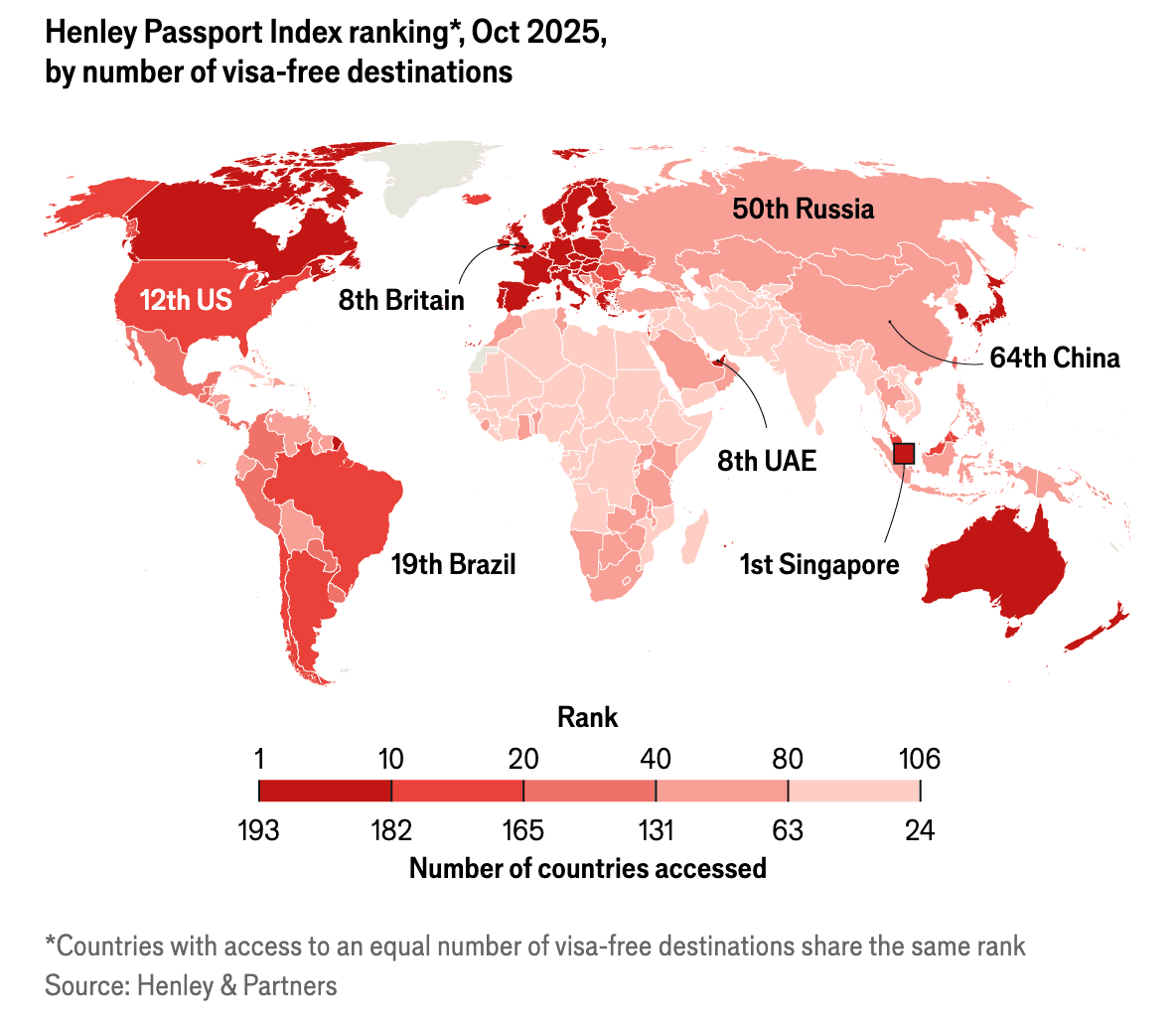

This week's bonus section covers our selected chart of the week. Labour mobility is an important aspect of globalisation and supports labour markets around the world. Ensuring that visa systems and passports are effective is imperative to allowing labour to flow around the world. As shown below, our chart covers the Henley Passport Index ranking for 2025[17].

As you can see the top ranks are focused around the highly developed regions within Asia, Europe and North America. This provides these countries with easier access to highly-skilled and educated labour, along with facilitating more cross-border investment, such as Singapore, which is a highly multicultural country. It is also extremely important for the businesses of these countries. The recent decision over H1-B visas in the US are likely to affect many businesses in the Silicon Valley area, which rely on overseas skilled workers. This contrasts with China (currently a mere 64th in the ranking) who have recently announced a K-visa scheme to attract technology workers to China[18].

In a current state of de-globalisation, many nations are experiencing political polarisation over migration issues, and this a highly debated topic, however there is no question around the importance of passport and visa strength in supporting a country.

Editors: Liam Sanderson, Dinel Gamage

Writers: Liam Sanderson, Filip Wang, Cleo Vuillot, Harshil Nichani

References:

[1] American Action Forum - https://www.americanactionforum.org/insight/tracker-the-federal-reserves-balance-sheet/

[2] Reuters - https://www.reuters.com/business/feds-powell-say-end-balance-sheet-drawdown-may-be-nearing-2025-10-14/

[3] Financial times - https://www.ft.com/content/53827239-849e-466f-a680-babf8fbefe7d

[4] Fintech future: S&P Global to acquire With Intelligence for $1.8bn - https://www.fintechfutures.com/m-a/sandp-global-to-acquire-with-intelligence-for-1-8bn

[7] Financial Times - https://www.ft.com

[8] AP News - https://apnews.com

[9] Reuters - https://www.reuters.com

[10] The Guardian - https://www.theguardian.com

[11] Times of India - https://timesofindia.indiatimes.com

[12] MSCI Official Statements - https://www.msci.com/news-and-research/press-releases

[13] Financial Times - https://www.ft.com/content/2abf7ace-f7ef-41da-be80-8fe07bbe4a87

[14] CNBC - https://www.cnbc.com/2025/10/16/spotify-ai-music-sony-universal-warner.html

[15] Netflix - https://www.netflix.com/tudum/articles/netflix-spotify-video-podcasts

[16] Financial Times - https://www.ft.com/content/be3f6853-286b-4296-9cef-fd0a9da624f8

[17] Economist - https://www.economist.com/graphic-detail/2025/10/16/the-worlds-most-and-least-powerful-passports

[18] Financial Times - https://www.ft.com/content/01a0029c-9f7c-4b31-a120-d1652f198448

[19] Financial Times - https://www.ft.com/content/9426937e-28d3-4846-8440-c30583524d4c